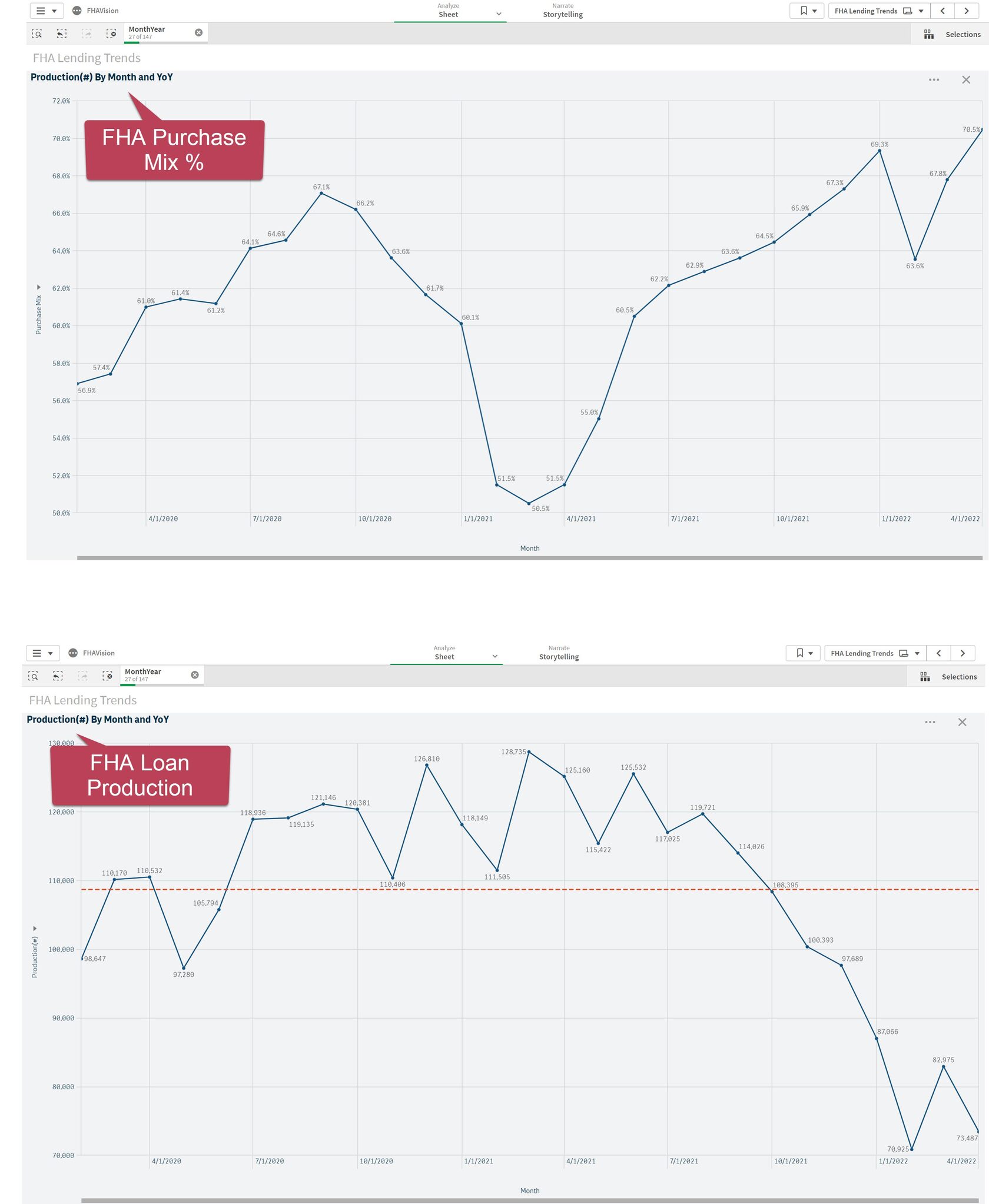

In April 2022 overall FHA production was 73,487 originations, down from 125,160 in April 2021. FHA purchase loans have shown a bit more resilience than refi, with April FHA purchase 21% below its 12-year average, while April FHA refi is 35% below its own 12-year average. The charts below show first the purchase % of total FHA loans (the purchase mix), following by all FHA loans, over the past 2 years:

It's important to remember in this context that because of its terms (i.e. 580 minimum credit score and 96.5% LTV), FHA loans are often used by first-time homebuyers.

In general, the FHA program does not allow borrowers to purchase or refinance a second residence or to use FHA to purchase or refinance investment properties. But there are some exceptions. An FHA loan can be used to purchase up to a four-unit dwelling, as long as the borrowers live in one unit as their primary residence. Then they can rent out the other units for income. In fact, in 2021, $1.7 Billion in FHA loan volume for the purchase, refinance, or home improvement of 1-4 unit investment properties were originated (source: Polygon Research, HMDAVision).

Lenders who offer FHA loans are poised to capture important purchase mortgage opportunities in a very tight mortgage market. These lenders may also be able to expand their customer base in low– and moderate-income communities and to a broader range of borrowers.

For more information, visit www.polygonresearch.com.