In declining mortgage lending markets, lenders typically look for niche opportunities for growth. One such niche is the home improvement segment.

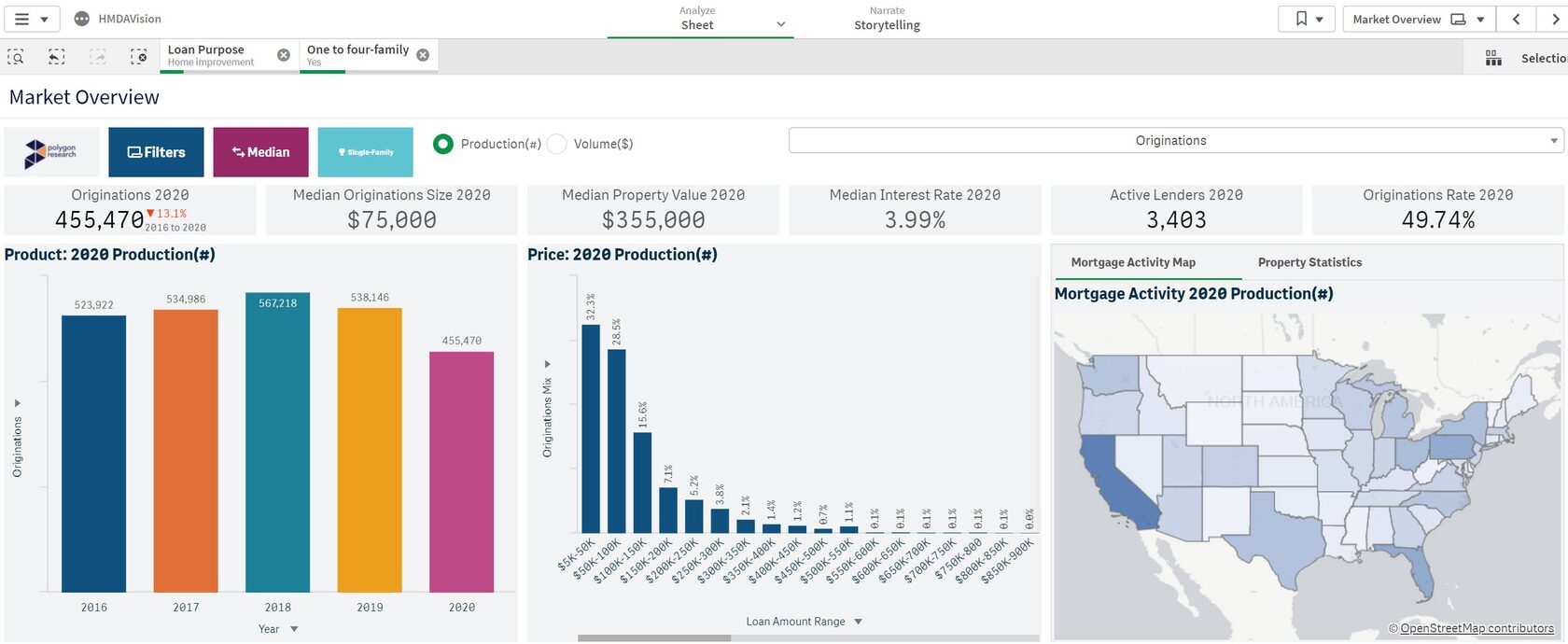

From 2016 through 2020, the annual home improvement mortgage production ran around 524,000 loans on average. As interest rates fell in 2020, home improvement loan production decreased to about 455,000 loans (see figure 1 below). In 2020, the size of the home improvement lending segment (for 1-4 unit properties) was $52.3 Billion; the median home improvement loan was $75,000, which was higher than the median home improvement loans size of $50,000 in 2016.

Figure 1: Overview of Home Improvement Mortgage Market

How can you size up the home improvement lending opportunity for your market?

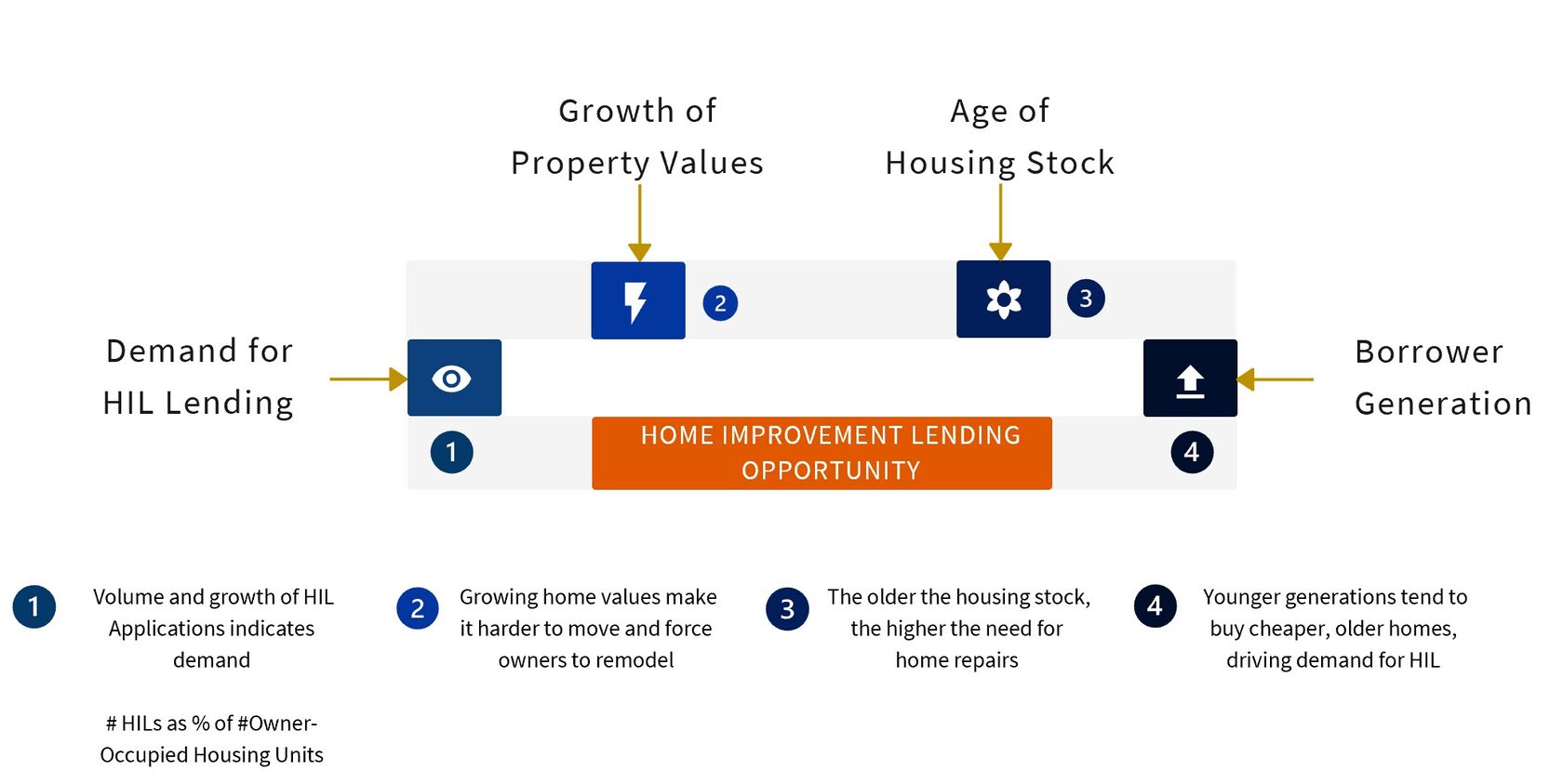

Before you embark on this project, you should first review and clarify your market territory definition and boundaries. When sizing up the home improvement lending opportunity in your local market, we recommend that you carefully analyze and take into consideration 4 distinct factors as illustrated in the figure below.

Figure 2: Methodology for Estimating Home Improvement Opportunity

Factor 1: Demand for home improvement lending

An estimate for the demand for home improvement loans are the applications taken and their growth year-over-year. A reliable and consistent source of data for this is the HMDA LAR, which we model in our HMDAVision app. You get the entire "mortgage market on a silver platter" as one of our happy users told us, and with a couple of filters, you can zero in on the answer you are looking for.

Factor 2: Growth of Property Values

As property values appreciate, many people choose to stay put and remodel their homes instead. The higher the home values, the higher the demand for home improvement loans. This factor is location-based and careful analysis of your market should be done.

Factor 3: Age of Housing Stock

The older the housing stock, the higher the need for home repairs. One reliable source of data on age of housing stock is the American Community Survey (ACS), which we model in our CensusVision app. Depending on the size of your market and/or the number of your locations, you can do your analysis in CensusVision within minutes.

Factor 4: Borrower Generation

Younger generations tend to buy cheaper, and often older homes, driving demand for home improvement loans. We recommend blending two data sources for that, easily accessible through our HMDAVision and CensusVision apps. It's easy to do analysis and to plan your sales/marketing strategy in our apps because we model demographics and housing data together with lender and geo-location data.

In subsequent posts we'll discuss the type of mortgages used to finance home improvement projects. The 2021 HMDA LAR data is coming in a few weeks, and our HMDAVision app will be updated with 2021 data. And CensusVision is updated monthly. Sign up to receive our blogs right into your inbox and to keep ideas and perspectives flowing into your organization, and/or schedule a 15-minute free brainstorming session with us.