HMDA, the Home Mortgage Disclosure Act, is disclosure legislation - implemented via Regulation C - aimed at ensuring fair and effective mortgage lending in the US. One of the particular strengths of the HDMA data is that it shows the full lifecycle of mortgage applications.

The Action Taken field shows whether the outcome of the application, if not a purchased loan, was:

- Originated

- Approved but Not Accepted

- Denied

- Withdrawn

- Closed Incomplete

- PreApproval Denied

- PreApproved Not Accepted

Once on the books, the HDMA data also shows which loans are then sold and to which investors.

Why is this important?

Going beyond fair Lending compliance use case, these data points can be modeled to measure the Pull-Through Rate, i.e. the percentage of loans applied for that are closed and funded by the lending institution. This KPI is an important measure of efficiency and overall customer service levels. Pull-Through Rate is a lagging indicator of possible inefficiencies of the mortgage production process, for example:

- Extended cycle times for underwriting, borrower data collection, and closing.

- Excessive underwriting touch points.

- Lack of competitive rates and incentives for potential borrowers.

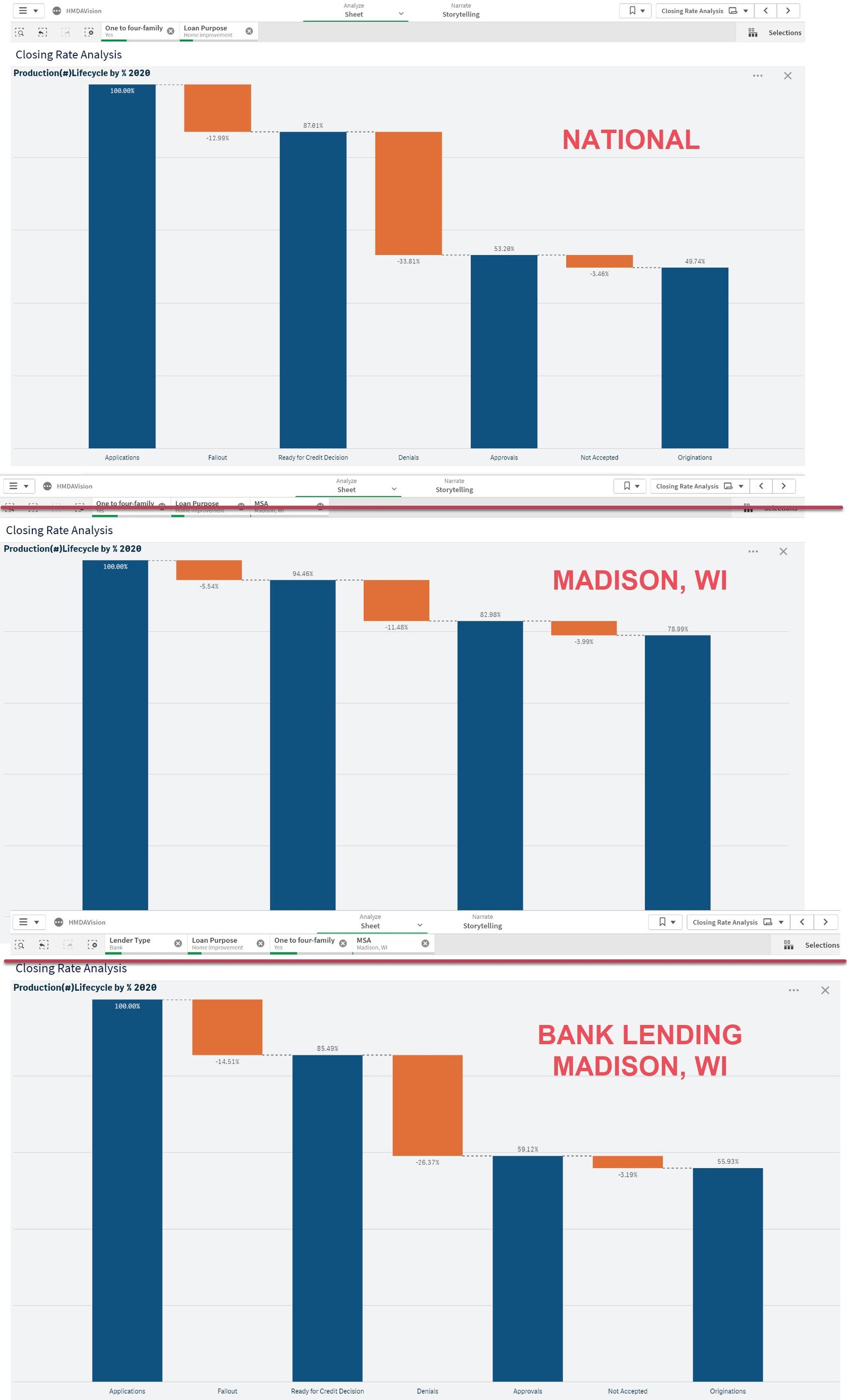

In HMDAVision, you can calculate this KPI instantly at any geographic level, for any loan product, for your peers/competitors, including measure it by demographic group, etc. As illustrated below, the pull-through rate at the national level for home improvement mortgages is 49.74%, but in Madison, WI MSA, it is almost 79%. Then, applying a filter for a group of lenders (for example banks), this KPI decreases to 55.93% for Madison. You can isolate only your organization's pull-through rate to benchmark it against the market. Furthermore, you can continue to explore this pull-through rate by loan type, by census tract, and by other features of the mortgages you have originated in this market and for the full spectrum of your borrower demographics.

This instant filtering and recalculation made possible in HMDAVision allows you to benchmark your overall performance against peers and market and to connect the dots. For example, if you have a low pull-through rate compared to your competitors, you may have a situation where your LOs, underwriters, and processors are spending a lot of time on loans that never close. Use it to find inefficiencies and bottlenecks in your mortgage production process.

Schedule a 15-minite data discovery to see your pull-through rate in any market.