FHA purchase lending has been overlooked as a viable mortgage credit option in high-cost areas. Over the last decade, FHA purchase lending has indeed declined in terms of volume and loan production in high-cost areas. Yet, some lenders like United Wholesale Mortgage, Rocket Mortgage, Genhome Mortgage Corporation, Loandepot, and Caliber Home Loans, are growing their FHA purchase loan volumes in California's high-cost areas and putting families into homes.

The borrowers of FHA purchase loans in CA's high-cost areas are typically young - about 40% of FHA purchase loans are made to borrowers 34 years or younger (source: Polygon Research, HMDAVision). While FHA purchase lending has been declining overall, when we segment by applicant's age, we see a healthy growth year-over-year for FHA purchase lending in high-cost areas (CA example).

What are the limits for FHA loans in high-cost areas?

The FHA national high-cost area mortgage limits are set at 150 percent of the national conforming limit of $647,200 for a one-unit Property. In 2022, the high-cost areas limits are:

- 1-unit: $970,800

- 2-unit: $1,243,050

- 3-unit: $1,502,475

- 4-unit: $1,867,275

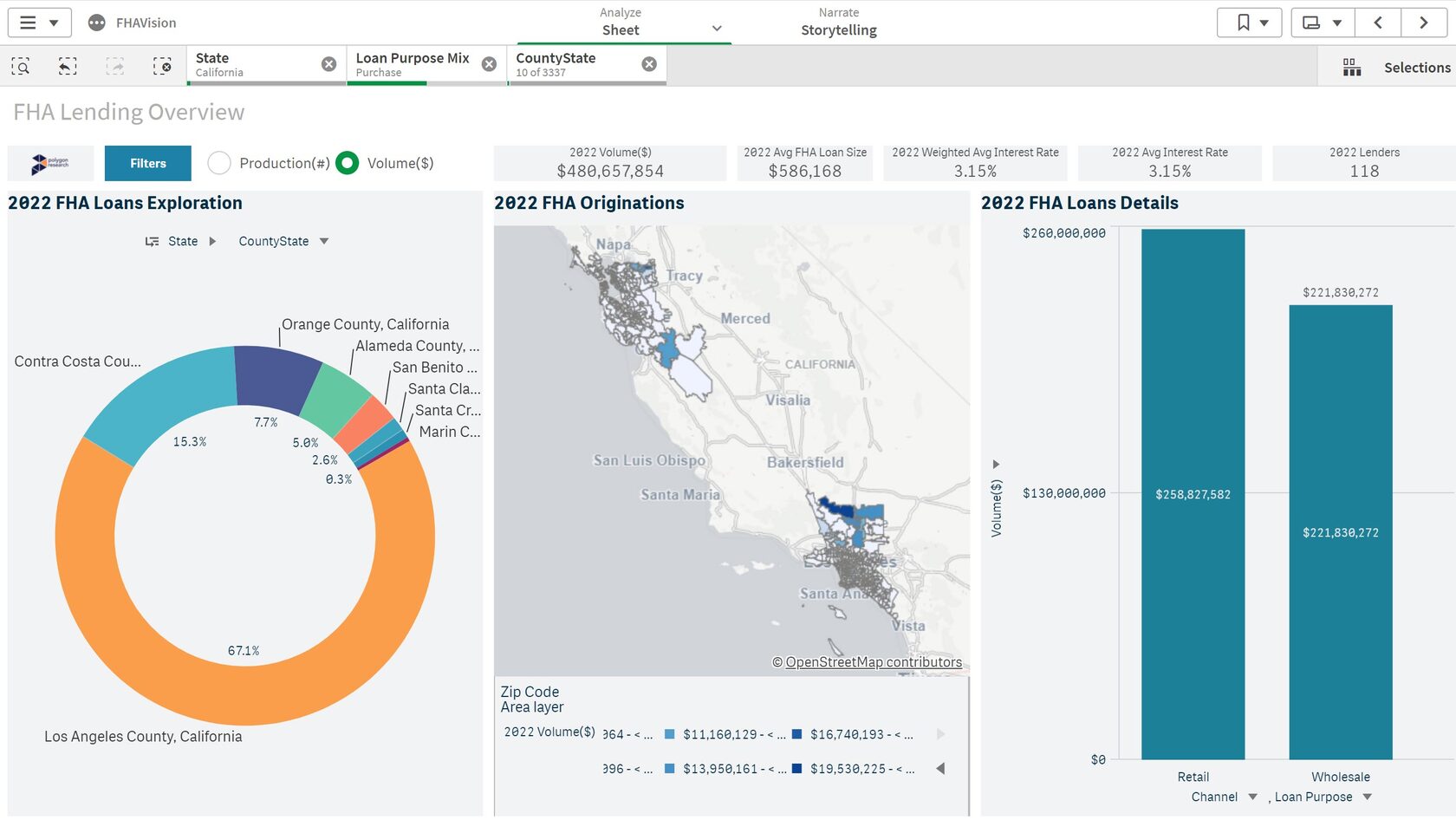

To measure and estimate FHA lending in high-cost area, we used single-family FHA endorsement data we've modeled in our app, FHAvision. We focused on high-cost areas at ceiling in CA as a focus for our quick market analysis - see a snapshot of the dashboard below.

FHA purchase lending in high-cost (at ceiling) areas in CA was about $481 Million in January 2022, which is 30% of all FHA purchase lending in the state (about $1.62 Billion, January 2022 YTD). And the top 3 counties by FHA purchase lending volume in high-cost areas in CA are:

- Los Angeles

- Contra Costa

- Orange county

Understanding the top geographies is important when crafting a mortgage sales growth strategy because they indicate where lenders were most successful in funding FHA purchase loans despite the headwind of high home prices. Such an analysis also points to the presence of real estate agents who are comfortable working with FHA lenders. FHAvision allows for further drilling to identify even more granular geographies such as zip codes.

Another important factor for sales growth strategy in FHA lending in high-cost areas is the role of the wholesale channel (brokers). As the dashboard shows, about 46% of the FHA purchase volume (~$221.8 million) in these high-cost areas was originated through the wholesale channel. In this case, developing trusted relationships with brokers would be an essential element in the lender sales growth strategy. Further analysis of the brokers in these high-cost areas can be performed in FHAvision.

In 2022, finding niche lending opportunities, especially in purchase mortgage lending, can be an important strategic lever to set lenders apart. If you would like to explore your high-cost area and brainstorm your growth strategy, schedule a 15-minute free and interactive demo with us.