POLYGON RISK

Prepayment & Credit Performance Platform (CPR & CDR)

Polygon Risk models and predicts prepayment (CPR) and default (CDR) — so you can quantify mortgage performance risk at the loan, cohort, and seller level.

Mortgage risk models need a reset.

Legacy systems rely on lagging data, black-box logic, and blended averages that hide what’s really happening in your portfolio.

Fragmented Risk Signals

Performance, origination, and macro indicators live in separate systems and refresh on different schedules. By the time you see the risk, the market has already moved.

Polygon Risk unifies loan-level, HMDA, MBS, and macro data in one continuously updated modeling layer.

Black-Box Models with No Explainability

Most vendors hand you a number, not a narrative.CPR and CDR outputs are opaque - impossible to audit, justify to ALCO, or defend to regulators.

Polygon Risk provides transparent, explainable ML models built from observable loan-level features, so you always know what’s driving risk.

Portfolio Averages Hide Real Exposure

Blended portfolio metrics flatten key differences by seller, channel, product, FICO, LTV, and geography. You end up managing to an average instead of managing true concentrations.

Polygon Risk models at the loan and cohort level to surface hidden pockets of prepayment and credit risk.

Predictive Without Descriptive = Blind Bets

Forecasts without a solid descriptive base mislead decisions. Descriptive dashboards without forward views keep teams stuck in hindsight.

Polygon Risk merges descriptive analytics and predictive modeling (CPR + CDR) so you see what happened, why it happened, and what’s next.

Together, these four problems define the gap between legacy risk systems and modern mortgage intelligence.

Polygon Risk closes that gap.

Transparent and Explainable

Our models are fully auditable. Every CPR/CDR prediction includes feature importance, model diagnostics, and historical context—so you can defend results to ALCO, auditors, and regulators with confidence.

Open-Data Foundation

No proprietary black boxes or restricted APIs. Polygon Risk is grounded in publicly available, verifiable data from HMDA, the GSEs, GNMA, Census, and FEMA—integrated into a consistent modeling framework.

Granular and Flexible

Model risk at any level of detail—from loan and cohort to seller, product, or investor. Slice by credit score, LTV, geography, or channel to reveal hidden exposure and opportunity.

Independent and Affordable

Not tied in to any one investor, or servicer. That independence means unbiased modeling and pricing designed for accessibility—not enterprise lock-in.

Predictive intelligence

Polygon Risk brings together descriptive analytics and predictive modeling in one transparent platform—so you can understand today’s exposures and anticipate tomorrow’s outcomes.

Unified Data Foundation

We integrate agency MBS loan-level data, HMDA origination records, FEMA and Census datasets, and macro-economic indicators into one consistent, normalized data layer. No silos. No vendor lock-in. Every metric you see ties back to verifiable open data.

Dual Model Engine — CPR & CDR

Polygon Risk models both voluntary and involuntary prepayment risk.

CPR Model predicts borrower behavior - refinance, turnover - under changing rate and credit conditions.

CDR Model captures credit deterioration and involuntary prepayment (default, foreclosure) using loan-level performance and macro signals.

CPR Model predicts borrower behavior - refinance, turnover - under changing rate and credit conditions.

CDR Model captures credit deterioration and involuntary prepayment (default, foreclosure) using loan-level performance and macro signals.

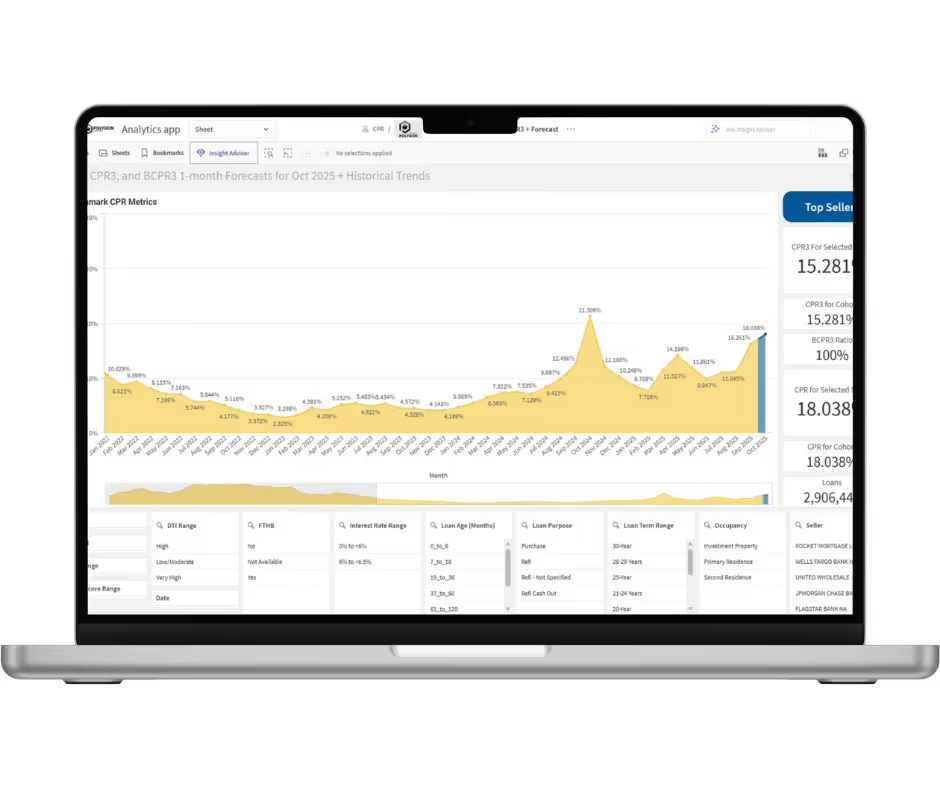

Cohort and Seller-Level Forecasts

Unlike one-size-fits-all models, Polygon Risk outputs predictions at the cohort level—by seller, channel, product, FICO band, LTV, occupancy, and region.You can roll up to portfolio or investor view in seconds.

Every prediction comes with feature importance, model confidence, and historical context.

You don’t just get a number—you see the story behind it.

You don’t just get a number—you see the story behind it.

Frequently asked questions

About Polygon Risk

What is Polygon Risk?

Polygon Risk is our risk intelligence suite for mortgage and housing portfolios. It is designed to help teams quantify risk drivers—starting with climate and disaster exposure—and connect those risks to market, borrower, and loan performance context. Polygon Risk is actively being built, with capabilities released in stages.

What apps are included in Polygon Risk?

Polygon Risk includes TerraVision for climate and disaster exposure analysis, along with CPR and CDR modeling capabilities built on loan-level agency MBS and performance data. These tools are designed to work together so teams can connect geographic exposure, borrower/loan characteristics, and observed portfolio behavior over time.

What can Polygon Risk help you do?

Polygon Risk helps you identify where risk is concentrated, how it varies by geography and borrower context, and what exposures could matter most for underwriting, portfolio monitoring, servicing strategy, and planning. The goal is practical: clearer risk signals earlier, grounded in data you can explain.

What data does Polygon Risk use?

Polygon Risk blends hazard and vulnerability datasets (including FEMA’s National Risk Index) with housing and demographic context (Census/ACS) and loan-level agency data. For performance and modeling, it uses loan-level agency MBS and loan-performance data across the three agencies to analyze prepayment (CPR), credit performance (CDR), and how risk varies by geography, borrower profile, and product characteristics.

Is Polygon Risk available now, and what’s coming next?

Polygon Risk is in active development. Current capabilities focus on disaster risk exposure and early performance modeling, with additional releases planned to support deeper segmentation, monitoring over time, and clearer links between risk exposure and mortgage market behavior. If you want to confirm what is included in your tier today, we can share the latest scope and release notes.

See How It Works

Discover how Polygon Risk turns billions of loan-level records into actionable insight.

Contact us to learn more

sales@polygonresearch.com